Precision Matters: Getting NOI Right

When it comes to investing in single-tenant net lease properties, one number has the power to shape everything: from what you offer on a property to how much income you expect to generate. That number is Net Operating Income (NOI).

At first glance, calculating NOI may seem simple: rent minus operating expenses. But for net lease property owners and buyers, especially in a market where cap rates are used to benchmark value, even a small miscalculation can skew results. It's a common scenario: investors often rely on figures provided in broker offering memorandums when making offers, only to discover later in the transaction that these figures were inaccurate or lacked crucial information.

This article breaks down what NOI really means in the context of net lease valuation, why accuracy is essential, and how to get it right. If you want to maximize returns and make informed acquisition decisions, this guide is for you.

Why NOI Is the Foundation of Net Lease Valuation

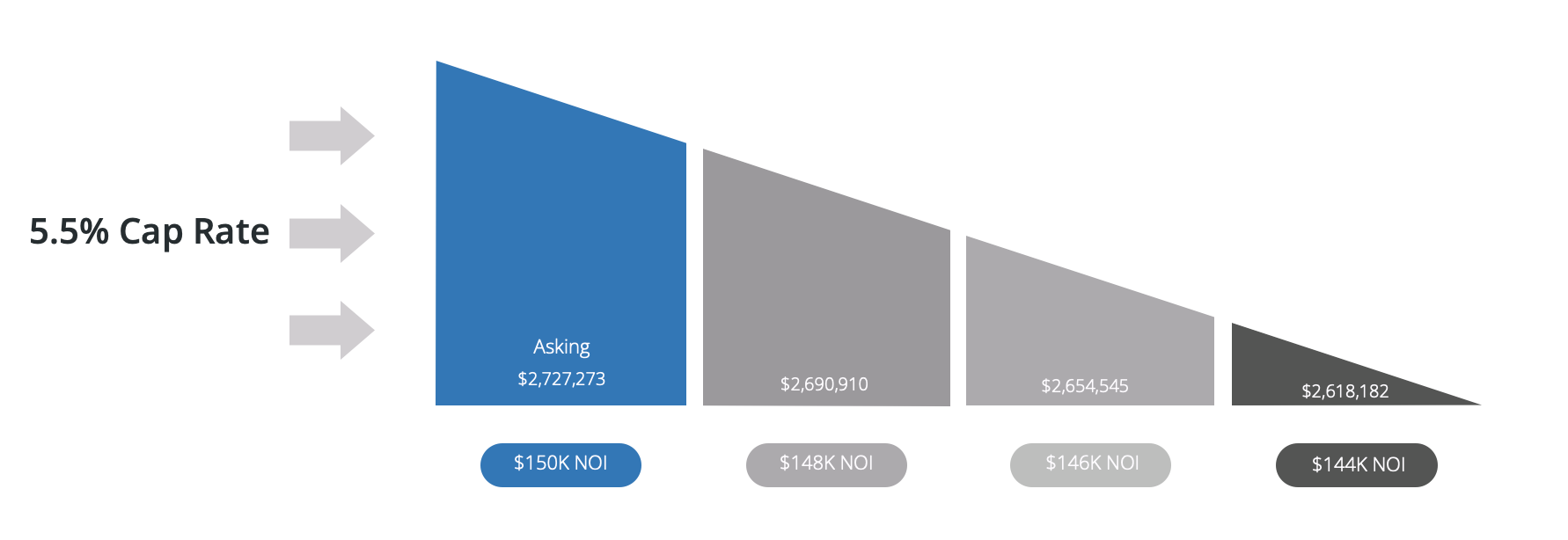

In single-tenant net lease investments, valuation is typically driven by the capitalization rate (cap rate) applied to a property’s Net Operating Income. The formula is:

Purchase Price = NOI/Cap Rate

This makes NOI the foundation of valuation. If your goal is to evaluate acquisition opportunities or price your property appropriately, even minor inaccuracies in NOI can add up fast.

The Tools to Calculate NOI Are Simple, but the Process Isn’t

A basic NOI formula subtracts operating expenses from rental income. For net lease investors, those numbers often appear in offering memorandums or spreadsheets. But that’s where issues arise.

Many investors assume the NOI figure they receive is accurate. In reality, we frequently find:

- Rent roll inconsistencies: Are rent commencement dates, base rent levels, and rental escalation dates correctly represented?

- Overlooked landlord obligations: Even in triple net leases, some repair and maintenance costs may fall on the landlord.

- Title and CC&Rs: Properties made part of a center or complex often require landlords to pay reciprocal maintenance fees, which may or may not be reimbursable depending on lease terms. These costs are common but rarely found in offering memorandums.

- Pass-through limitations: Leases may contain caps or timing restrictions on recoverable expenses, which limit full reimbursement.

- Insurance requirements: Leases may contain requirements that the Landlord carry its own liability insurance policy, and in many leases this cost is non reimbursable.

Without a clear understanding of the lease and how provisions impact income and expenses, NOI can quickly drift from reality.

How Small Errors Lead to Costly Impacts

Consider a brand new, 40,000 SF logistics property valued at $12,381,000 based on a reported NOI of $650,000 and a 5.25% cap rate. The lease is a fresh 15-year term to a high credit tenant, and everything appears clean on the surface.

However, during due diligence, the investor uncovers a common landlord-side obligation: the landlord must perform annual preventative roof maintenance to maintain the manufacturer’s roof warranty. This cost is $2,500 per year, and it is not reimbursable by the tenant.

While the original marketing NOI of $650,000 implies a value of $12.38 million at a 5.25% cap rate, the corrected NOI is actually $647,500. When you recalculate the property’s value using the updated NOI and the same 5.25% cap rate, the true value becomes approximately $12,333,333—a difference of $47,619.

This pricing gap is entirely due to a single, seemingly minor ownership obligation that was overlooked in the pro forma.

And the long-term impact?

Over a 5-year hold, the investor will pay $12,500 in unrecoverable roof maintenance. Combined with the $47,619 reduction in residual value, the total negative impact is over $60,000. In environments where pricing is tight and cap rates are compressed, small obligations like these can make the difference between meeting return targets and falling short.

Did You Know? A $2,500 annual expense—just over $200 per month—results in a nearly $47,000 valuation difference at a 5.25% cap rate. Small costs can create big gaps.

How This Analysis Can Strengthen Your Offer Strategy

Insights like these do not just help with post-acquisition budgeting. They can also be used to craft a smarter and more defensible offer. In this case, the buyer could reduce their offer price by $50,000 by citing the uncovered roof maintenance obligation and its impact on both annual cash flow and residual value. By presenting a clear breakdown of unreimbursed costs and aligning the offer with a corrected NOI and target cap rate, the buyer positions themselves as credible and informed. This approach protects investment returns and gives the seller a rational basis for considering the adjustment.

Key Practices to Get NOI Right

Producing a reliable NOI requires not only accurate data but also a disciplined, methodical review process. Follow these key steps to get it right:

1. Review the Lease, Not just the Offering Memorandum

Offering memorandums may overlook critical details. Read the full lease and all amendments to verify:

- Base rent schedule

- Escalation terms

- Operating expense responsibilities

- Expense reimbursement mechanics

- Insurance requirements

2. Verify Reimbursable Expenses

In a typical triple net lease, tenants are responsible for reimbursing the landlord for taxes, insurance, and maintenance. However, reimbursement is governed by the lease, and the actual recovery can vary widely depending on the terms.

Key items to verify:

- Are there caps on operating expense reimbursements?

- Are capital expenditures reimbursable, or explicitly excluded?

- Are administrative, legal, or management costs included in pass-throughs?

- Are there deadlines or timing restrictions on when expenses must be billed?

Even if an expense appears recoverable, missing a lease deadline or hitting a reimbursement cap can shift the burden to the landlord. Reviewing these provisions in detail is essential for accurate NOI analysis.

3. Review Unreimbursable Expenses

Some expenses, even in a triple net lease, are fully borne by the landlord. These may be clearly stated in the lease or implied by exclusion. Common examples include:

- Landlord’s liability insurance

- Preventative maintenance not covered by the tenant

- Costs related to shared facilities or reciprocal easement agreements (REAs)

These costs are not typically reflected in broker-provided NOI figures, but they reduce the true income an investor receives. While they may not affect valuation directly, they have a meaningful impact on cash flow and should be included in your pro forma analysis.

Conclusion

Net Operating Income is not just a number. It is the foundation of your entire net lease investment strategy. Getting it right means carefully reviewing lease terms, validating assumptions, and modeling real-world cash flow with precision. Getting it wrong can lead to inaccurate pricing, lower investment returns, and reduced cash distributions, often without investors expecting the impact.

Related Trinety Insights

Here are more articles to help you sharpen your NOI approach:

- Active vs. Passive Net Lease Management: Understand why NOI is not passive and why oversight matters

- What Triple Net Really Means: Unpack the NNN lease structure and avoid common misconceptions

- Approach to Capitalized Value: Understand how NOI, lease term, and cap rate expectations interact to determine property value—and why even small miscalculations can have long-term effects on investment performance.

Ready to shift from reactive to proactive management?

👉 Schedule a demo or sign up for Trinety today and take control of your net lease investments.